Financial or consumption data: When is a carbon footprint most meaningful?

May 19, 2022More and more companies have to deal with their carbon footprint. Some have to comply with legal requirements or participate in reporting programs such as the CDP, while others want to achieve carbon neutrality for themselves or their products and thereby also identify reduction opportunities, setting themselves a science-based target. Either way, they need to understand their carbon footprint to gain insight into how they can do better.

The standard for calculating carbon footprints, the Greenhouse Gas Protocol (GHG), lists various ways to create a footprint: a calculation can be based on consumption data, which provides high accuracy and robust results but requires a lot of effort to obtain the data. Alternatively, a calculation can also be based on financial data. It is easier to conduct but is much less accurate.

If companies want to use the carbon footprint as a starting point for reduction measures or carbon neutrality, the greatest possible accuracy and robustness of the data is necessary. Therefore, ClimatePartner recommends conducting a detailed, comprehensive and accurate carbon footprint based on consumption data. This article discusses whether there can still be reasons to conduct a footprint based on financial data.

The challenge of data availability

The accurate calculation of a carbon footprint based on consumption data is often a laborious project, as the lack of data availability in particular is a challenge for companies. It already starts with the definition of what is to be taken into account for a calculation in the first place, i.e., defining the system boundaries. In addition, some companies are not able to collect precise data for individual areas. For example, in purchased logistics or business travel, often only data on the respective expenses is available, while complete data on the means of transport used or the distance travelled is missing. To overcome this problem and also to minimize the effort necessary for data collection, some companies are turning to carbon accounting based on financial data i.e., expenditures or costs.

What exactly is financial carbon accounting?

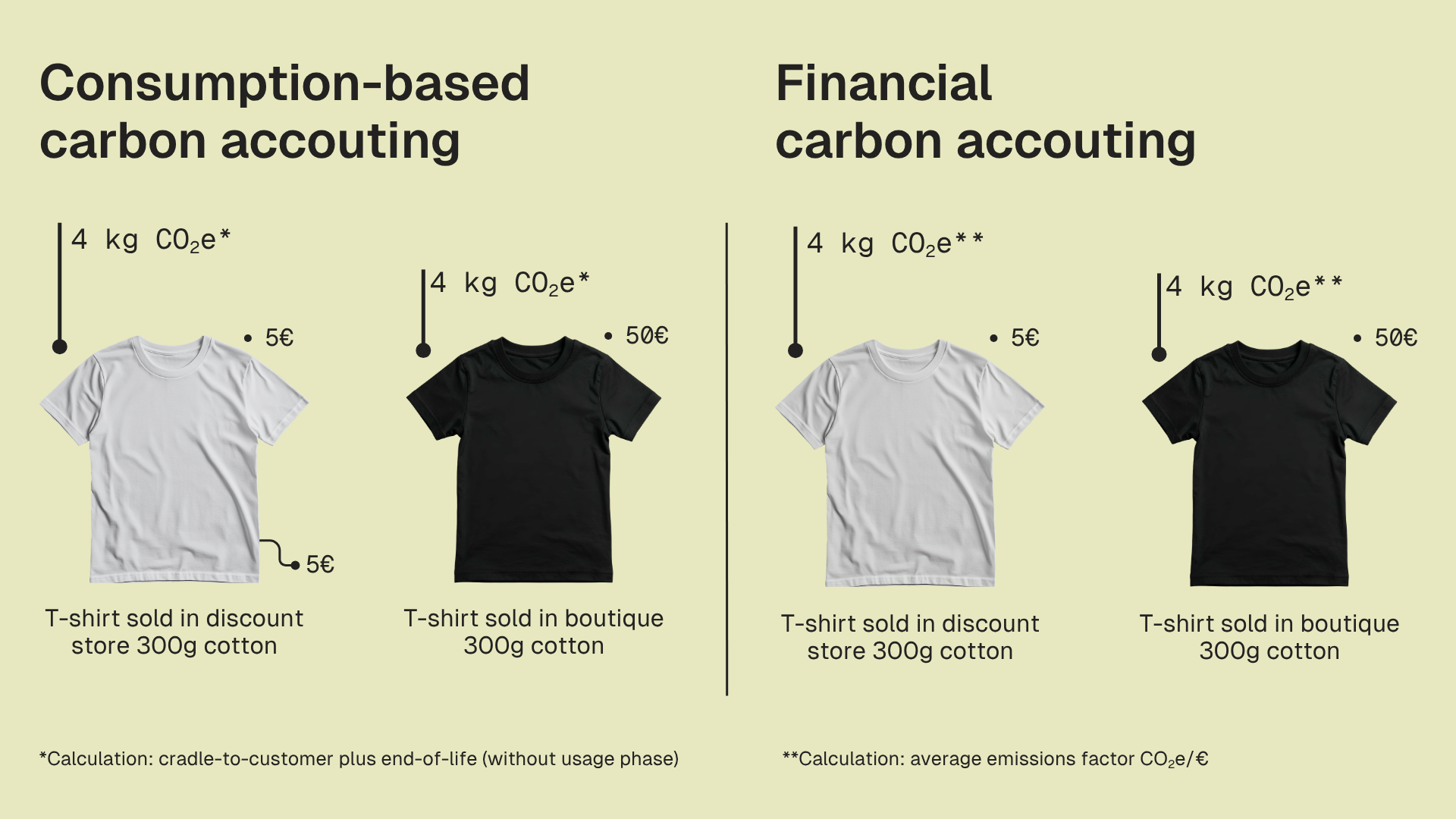

Carbon accounting based on financial data or spend costs estimates emissions based on the financial or economic value of a good or service. For this purpose, so-called emission factors are used, which indicate, for example, how many kilograms of carbon were caused per euro spent. Such calculations are based on so-called environmentally extended input-output (EEIO) models. Due to the easy availability of the data, which is usually provided by the company's financial or accounting department, this can be a time and cost-saving approach to creating a carbon footprint.

In contrast to calculations using consumption data — for example, the weight of purchased goods or fuel consumed — the cost-based calculation can be subject to strong fluctuations because it is linked to prices. Thus, for the same resource input, different prices between suppliers or a change in price automatically lead to a change in the emissions data, although the actual emissions remain unchanged.

For example, for identical t-shirts sold in a discount store for 5 euros each and in a boutique for 50 euros the calculated emission value would differ by a factor of ten – although the t-shirt is the same in both cases.

Carbon accounting comparison based on average values.

The current price increases for oil and gas would also lead to a significant increase in the emission figures for the same consumption. It is therefore not possible to derive reduction measures in any meaningful way. In addition, exchange rate fluctuations often cause errors in the application of the method. Another problem is that EEIO emission factors are much less in usage and thus less detailed, which is why, for example, it is often only possible to consider them for product categories (for example, a common emission factor for the category "food, beverages and tobacco"). In addition, such emission factors are updated only sporadically in many sources and are often outdated. Therefore, an expenditure-based calculation can at best be seen as a guideline.

How useful is the cost-based carbon footprint?

Especially if a carbon footprint is to serve as the basis for a climate action strategy, it is key that the footprint is able to verify the progress made. It would be a shame if these would remain invisible due to poor data quality. At the same time, it also must be avoided that poor data quality leads to the erroneous assumption that a reduction has been achieved. Since the cost-based method is subject to strong fluctuations, possible progress cannot be reliably assessed. Reduction targets should therefore always be set on the basis of consumption data. This is the only way to make a reliable statement. The GHGP also mentions the danger of incorrect prioritization when collecting data. Here, a calculation based on financial data can easily lead to wrong results: "Companies should be cautious when prioritizing climate action activities based on financial contribution, as expenditures and revenues may not correlate well with emissions." (Corporate Value Chain (Scope 3) Accounting and Reporting Standard, page 66). In addition, the standard indicates that such a cost-based calculation should be considered as screening only as it cannot replace the exact calculation for relevant items.

A complete calculation of a carbon footprint is often a costly project. The cost-based approach can be a suitable method to get a quick overview of the impact of different emission sources on the overall result. Such a screening is explicitly required, for example, by the Science Based Targets Initiative (SBTi) to get an assessment of all emission sources. In any case, however, large emissions sources should then be recalculated using consumption data for a more accurate result. A new calculation should also be carried out for smaller items when the calculation using consumption data is possible with a proportionate amount of effort. Only when items with low emissions impact and a large effort are to be calculated, the use of the expenditure-based method remains, provided that the data quality is improved in subsequent years and a switch is made to consumption data.

Cost-based calculations and the ClimatePartner label

When calculating a complete Corporate Carbon Footprint, ClimatePartner only uses the cost-based method if an initial assessment and screening of various emission sources is to be made. Wherever possible, a more detailed calculation based on consumption data is also performed in order to derive concrete measures for emission reduction.

In certain situations, it may be appropriate to calculate with financial data, at least for the time being. Nevertheless, climate action is only credible if a company assumes full responsibility for its carbon emissions caused, following the framework of carbon neutrality and applying concrete reduction strategies. This is only possible if actual consumption data has been calculated beforehand.

A calculation based on consumption data that is as accurate as possible is therefore a basic requirement for obtaining the ClimatePartner label for carbon neutrality. A calculation based on financial data is not sufficient for the label.