What is the CSRD and how will it affect your business?

February 26, 2026by Björn Bröskamp and Sibylle Simon

ClimatePartner published the first version of this article on 27 January 2022 and has updated it numerous times. It now reflects the current status as of February 2026.

The Corporate Sustainability Reporting Directive (CSRD) is the EU's new reporting guideline, set to replace the Non-Financial Reporting Directive (NFRD). It was proposed by the EU Commission in 2021 and will be applicable for the first time for the reporting of fiscal years beginning on or after 1 January 2024.

The new directive aims to significantly increase transparency in the field of sustainability. With it, more detailed reporting requirements will come into effect, making the CSRD an important element to be considered within a company's management reporting and business activities.

Who should be prepared for the new reporting?

The originally widened scope of the CSRD meant that instead of around 11,600 entities that reported their non-financial data, the new directive would ask nearly 50,000 businesses to report, with around 15,000 in Germany alone.

The EU omnibus regulation is a legislative proposal introduced by the European Commission in early 2025 to simplify and harmonise existing EU sustainability regulations. One of the most significant proposed changes in the omnibus is a narrowing of the CSRD thresholds: only large companies with more than 1,000 employees and net turnover exceeding €450 million remain within mandatory reporting obligations. This adjustment removes around 90% of previously in-scope companies from the CSRD requirements.

It is not only EU-based companies that need to pay attention to this change. The CSRD applies to any company with at least one large or listed EU subsidiary, or at least one branch with a net turnover of €450 million in the EU.

The regulations comes into effect in four stages, following delays from the omnibus:

- 1 January 2024: Companies already subject to the NFRD (reporting in 2025 on 2024 data).

- 1 January 2027: Large companies not previously under the NFRD enter the scope (“wave two”), reflecting a two‑year postponement introduced by the “Stop‑the‑clock” Directive for companies originally due to start with FY2025.

- 1 January 2028: Listed SMEs, small and non‑complex credit institutions, and captive insurance undertakings begin reporting (“wave three”); they retain the option to opt‑out until 2028 provided they explain the decision in their annual report.

- 1 January 2028: Large non‑EU companies with significant EU operations begin reporting (“wave four”).

How to publish sustainability information

With the new CSRD in place, sustainability reporting will be a mandatory part of management reports. Separate sustainability reporting will no longer be an option, as it is with the NFRD now. This means sustainability is seen as a strategic element of a company's business activities. This approach is greatly welcomed, since it gives sustainability topics the same prominence as financial reporting and no longer treats sustainability KPIs as measurements of a lower priority.

All relevant company information, including information on sustainability activities, will have to be published in management reports and must also be disclosed and accessible in a digital, machine-readable format.

CSRD reporting applies to all companies that fulfil the criteria mentioned above. A company is exempted from its publishing obligation only when it is part of a parent holding company and can instead refer to the parent company's report, provided that this report is in accordance with the EU reporting requirements. The exempted subsidiary company is then required to publish a consolidated management report of the parent company's reporting at group level. It is also required to include a reference to the fact that the company in question is exempted from the requirements of the Directive. For all reporting companies, an external audit will be mandatory to provide limited assurance of the report.

What information needs to be disclosed

The CSRD establishes the legal framework for sustainability reporting, while the European Sustainability Reporting Standards (ESRS) define the detailed disclosure requirements. The 12 sector-agnostic ESRS were drafted by the European Financial Reporting Advisory Group (EFRAG) and submitted to the EU Commission on 22 November 2022. The first set of standards was adopted by the European Commission in July 2023 and is now mandatory for all companies in scope of the CSRD.

The aim is to bring the ESRS broadly in line with international reporting standards and existing sustainability reporting standards, such as those of the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), the Carbon Disclosure Project (CDP), and others. Some of these standards also refer to the Greenhouse Gas Protocol. The CSRD and ESRS are also intended to be aligned with the EU Taxonomy.

In November 2025, EFRAG submitted amended ESRS to the European Commission for approval as part of the EU omnibus simplification process. Key updates include:

- An over 60% reduction in mandatory data points, with voluntary data points removed

- A more streamlined double materiality assessment

- Greater integration with other frameworks, including IFRS S1, IFRS S2, and the Greenhouse Gas Protocol, to reduce redundancies

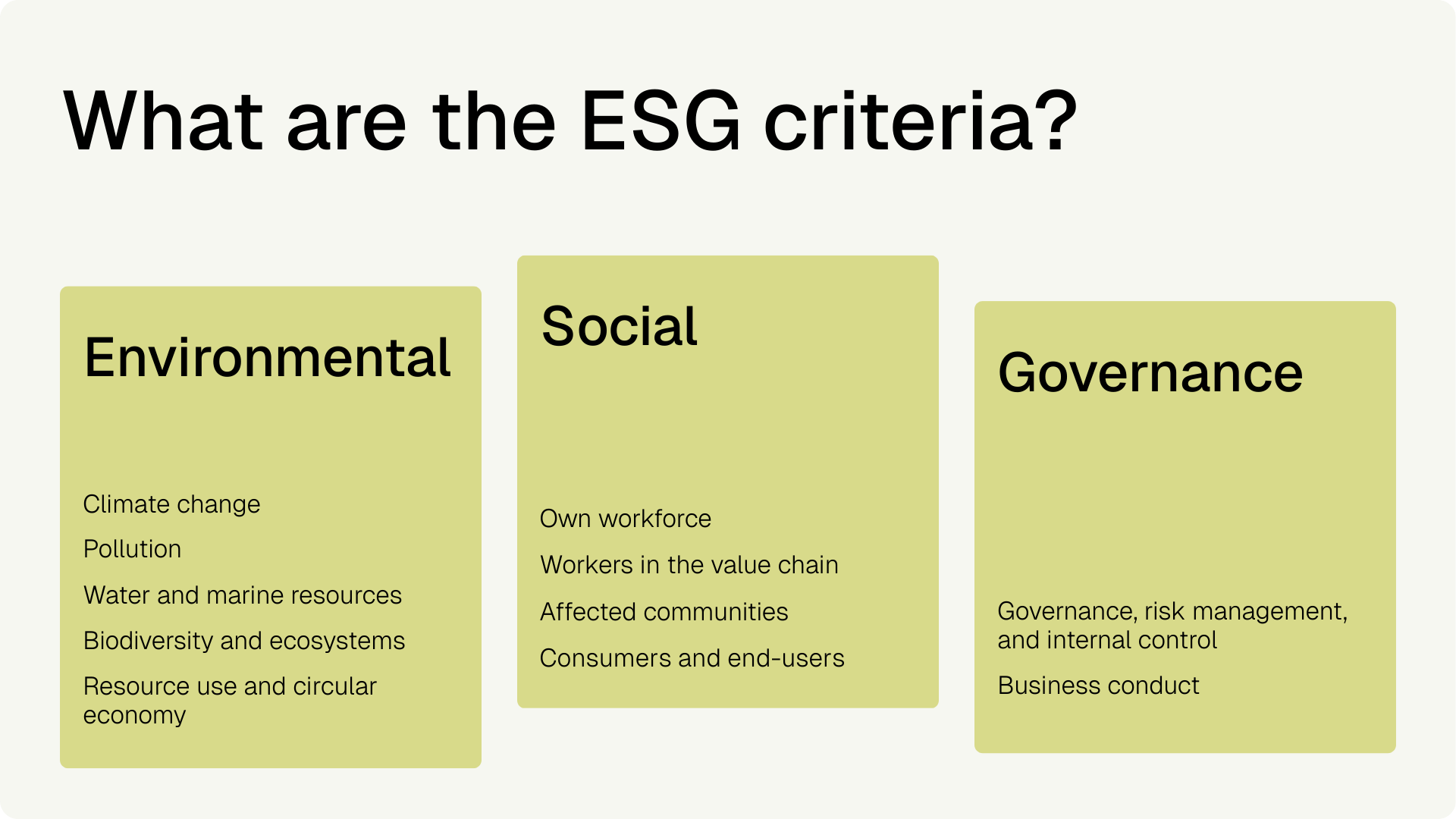

The Directive stipulates that the following environmental, social, and governance (ESG) aspects be considered when drawing up the reporting standards. They have each been compiled by EFRAG in the 12 reporting standards:

Another requirement of the CSRD is the principle of double materiality. This principle asks companies to report from two different perspectives: how each sustainability aspect affects the company (the "outside-in" perspective) and how each reporting aspect of the company affects people, stakeholders, and the environment (the "inside-out" perspective). With that, the current comply-or-explain approach of the NFRD will no longer be applicable.

ClimatePartner supports you in complying with the CSRD

Companies can seek support in complying with the new reporting requirements from external experts such as ClimatePartner. As carbon accounting will be a focus of future reporting, ClimatePartner is ideally placed to share its expertise. The various calculations of the carbon footprint of companies, products, and services, as well as the corresponding reports, will be able to be included in CSRD reporting. We also support our clients in defining clear climate action strategies and aligning them with the requirements of the Science Based Targets initiative (SBTi) and, in the medium term, with a net zero strategy. Such strategies, developed in cooperation with our consulting teams, can also be integrated into compliant sustainability reports.

CSRD and ESRS: How will your business be affected?

With the CSRD, carbon data becomes a crucial reporting element for companies.

Download the e-book to learn whether your company has a CSRD obligation, especially post-omnibus, and what you need to consider for your non-financial reporting.

Download for free