Corporate Sustainability Reporting Directive (CSRD)

What is the CSRD?

The Corporate Sustainability Reporting Directive (CSRD) is a new company reporting requirement designed to enhance the quality, consistency, and comparability of sustainability reporting by companies operating in the European Union (EU). It was proposed by the European Commission in 2021 to replace the Non-Financial Reporting Directive (NFRD). The CSRD was adopted in 2023, with the first companies reporting from 2024/2025.

The CSRD makes carbon data a crucial reporting element. From 2024 onwards, more businesses will be required to report more comprehensive and detailed information on sustainability. The main objectives are to improve the relevance and reliability of sustainability information, provide a comprehensive view of a company's sustainability performance, and foster sustainable investment and decision-making.

In 2025 the EU introduced omnibus legislation to overhaul sustainability standards following the EU Competitiveness Compass. This omnibus greatly affects the scope and implementation of companies complying with the CSRD.

Who does the CSRD apply to?

Companies that fulfil at two conditions will have to comply with CSRD (post-omnibus):

- over 1,000 employees

- over €450 million revenue

It is not only EU-based companies that need to pay attention to this change. The CSRD applies to any company with at least one large or listed EU subsidiary, or at least one branch with a net turnover of €450 million in the EU. The EU subsidiary or branch is responsible for CSRD-compliant reporting.

When does the CSRD take effect?

The CSRD was adopted by the European Parliament in November 2022 and came into force in January 2023. Following the omnibus and “Stop-the-Clock" directive, reporting for companies from the second wave on will be delayed by two years.

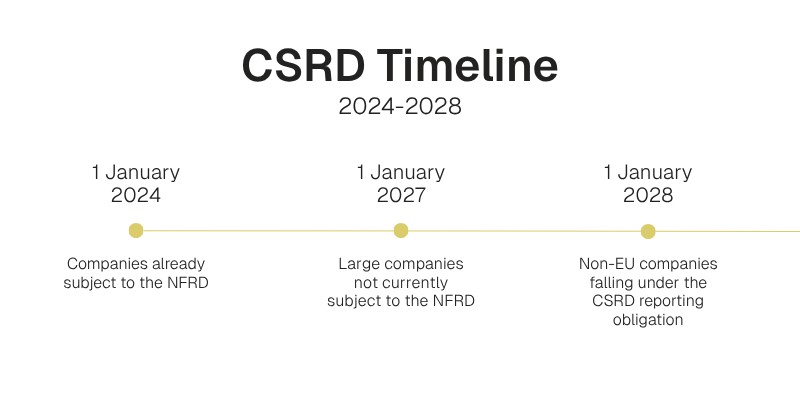

The regulations will come into effect in four stages:

- 1 January 2024: companies already subject to the NFRD

- 1 January 2027: large companies not currently subject to the NFRD

- 1 January 2028: non-EU companies falling under the CSRD reporting obligation

The Commission will review the standards every three years to consider new developments such as international standards.

What does the CSRD require?

Under the CSRD, climate action and transparent reporting on corresponding measures will become mandatory for companies. This gives sustainability strategy the same prominence as financial reporting.

The CSRD introduces a broad set of sustainability topics that companies need to report on. This includes environmental, social, and governance (ESG) factors, such as climate change, biodiversity, human rights, and anti-corruption measures. It emphasises forward-looking information to assess companies' long-term sustainability strategies.

What does the CSRD mean for your business?

The new directive will advance climate action, promote trust, and create a positive incentive for all companies to take responsibility. As one of several legislative initiatives, the CSRD provides both more clarity and more recognition of companies' commitment to climate action.

ClimatePartner supports you with your CSRD and ESRS E1 reporting.

CSRD and ESRS: How will your business be affected?

With the CSRD, carbon data becomes a crucial reporting element for companies.

Download the e-book to learn whether your company has a CSRD obligation, especially post-omnibus, and what you need to consider for your non-financial reporting.

Download for free