Scope 3 emissions

Scope 3 emissions definition

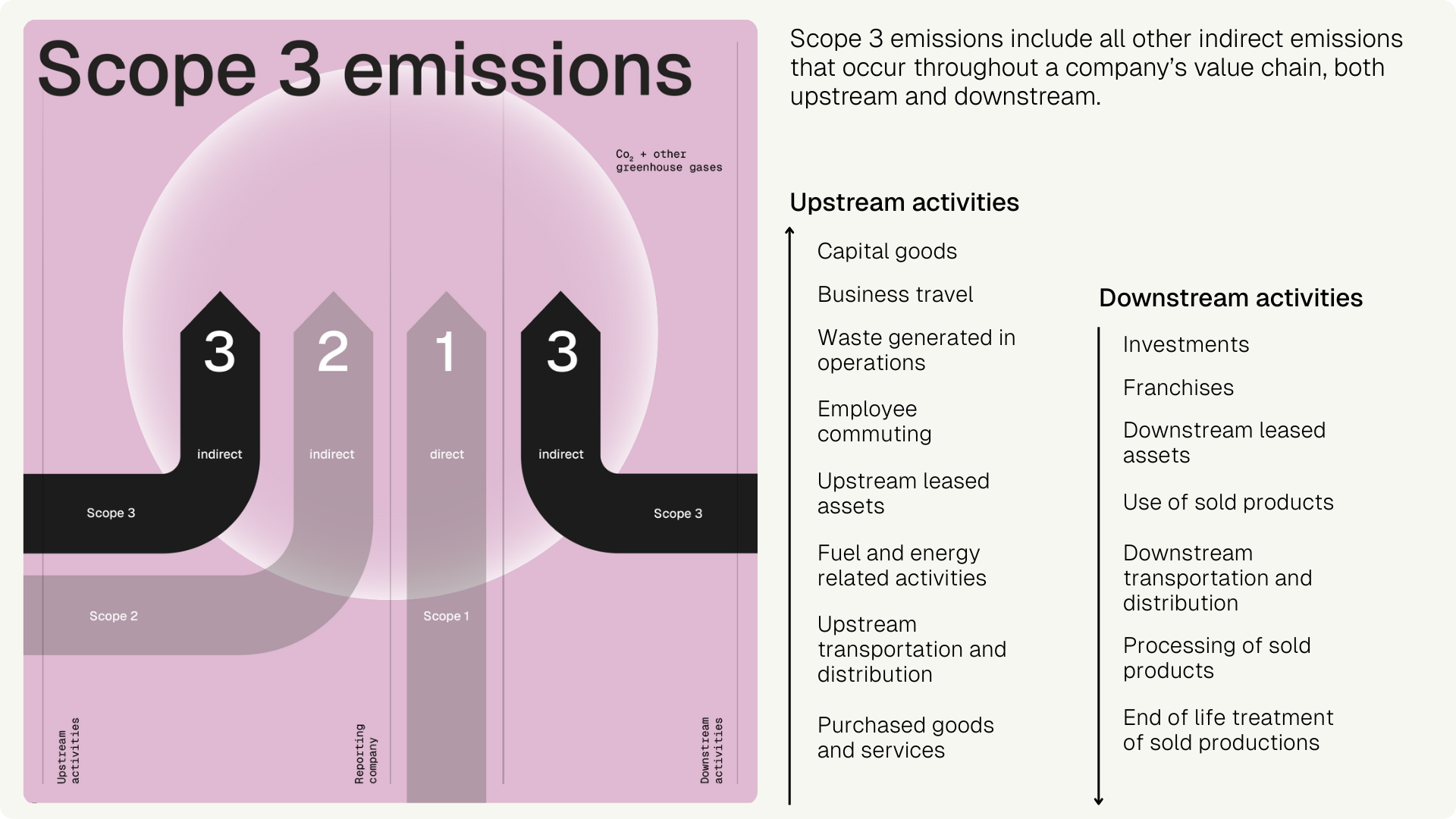

Scope 3 refers to the third and broadest reporting category of the Greenhouse Gas Protocol. This scope encompasses all indirect greenhouse gas (GHG) emissions from a company’s activities, occurring from sources it does not own or control.

Scope 3 usually makes up the greatest share of a company’s carbon footprint, covering emissions associated with activities up and down the value chain, like transport and distribution or the disposal of goods or services after they reach the consumer. Other examples of scope 3 activities include the extraction and production of purchased materials and the eventual use of sold products and services.

Scope 3 emissions categories

The GHG Protocol divides the emissions reportable under scope 3 into upstream and downstream emissions, classifying them into 15 categories. Not every category is relevant for every company, but knowing and understanding them is useful when devising effective reduction strategies.

Scope 3 encompasses indirect emissions from upstream and downstream activities

Upstream emissions

Upstream emissions relate to purchased or acquired goods and services and are generally generated from cradle to gate. The eight upstream categories are:

1. Purchased goods and services: Emissions from the production of purchased goods and services, e.g. the extraction and processing of raw materials. This category also includes electricity consumed through upstream activities, as well as transport between suppliers. For most companies, this is the single largest category (Scope 3.1).

2. Capital goods: Emissions from the production of capital goods purchased by the reporting company, e.g. equipment, machinery, buildings, facilities, and vehicles.

3. Fuel- and energy-related emissions: Emissions from fuel- and energy-related activities, including the extraction, production, and transport of fuels consumed by the reporting company. This includes coal mining, the refining of crude oil into petrol, the transport and distribution of natural gas, and the production of biofuels.

4. Upstream transportation and distribution: Emissions from the transport and distribution of products and services purchased by the reporting company, in vehicles and facilities neither owned nor operated by the company. This includes all freight types and the storage of purchased products in warehouses, distribution centres, and retail facilities.

5. Waste generated in operations: Third-party emissions from the disposal and treatment of waste and wastewater arising from operational processes owned or directly controlled by the reporting company.

6. Business travel: Emissions from the transportation of employees for business purposes in vehicles owned or operated by third parties, e.g. aeroplanes, trains, buses, and cars.

7. Employee commuting: Emissions from the transportation of employees commuting to and from work in vehicles owned or operated by other companies.

8. Upstream leased assets: Emissions from the operation of fixed assets leased by the reporting company, e.g. office buildings.

Downstream emissions

Downstream emissions include indirect GHG emissions related to sold goods and services. These emissions occur after the product leaves the company’s control. There are seven categories of downstream emissions:

9. Downstream transportation and distribution: Emissions from the transport and distribution of products sold to end consumers, in vehicles and facilities not owned or directly controlled by the reporting company.

10. Processing of sold products: Emissions from the processing of sold products by third parties (e.g. manufacturers) that must be further processed, transformed, or integrated into another product before use by the end consumer, e.g. agricultural or chemical products.

11. Use of sold products: Emissions from the use of sold products, e.g. the heat required to operate cooking or cleaning appliances.

12. End-of-life treatment of sold products: Emissions from the disposal and treatment of sold products using various waste disposal and treatment methods.

13. Downstream leased assets: Emissions from the operation of fixed assets leased by the company to third parties.

14. Franchises: Emissions from franchise operations.

15. Investments: Emissions from investments, including equity investments, loans, project finance, managed investments, and client services.

Is scope 3 reporting mandatory?

The GHG Protocol requires that companies account for and report all scope 1 and scope 2 emissions, but there is some flexibility in whether and how to account for scope 3 emissions. Scope 1 covers a company’s direct GHG emissions, while scope 2 accounts for the indirect emissions from the production of energy used in on-site operations. Scope 3 emissions are also a consequence of a company’s activities but occur from other sources along the supply chain. Essentially, scope 3 counts the scope 1 and 2 emissions of a company's suppliers and customers.

For example, a company’s externally purchased logistics are recorded under scope 3, as it is the logistics provider who is directly responsible for burning the fuel in the operation of its vehicles. For the logistics provider, these emissions would have to be recorded under Scope 1.

How to reduce scope 3 emissions

Scope 3 includes all indirect emissions that occur in the value chain of a reporting company. Even though these emissions are outside a company's direct control, they can still represent the largest portion of its greenhouse gas emissions inventory. Identifying and accurately calculating GHG emissions, especially for scope 3, is a complex task due to the numerous parties and processes involved.

The biggest lever often lies in scope 3.1 – purchased goods and services. Without supplier-specific data, companies have to rely on industry averages. These, however, reveal nothing about how a specific supplier produces, what energy they use or how efficient their processes are. Supplier-specific primary data is more reliable than estimates and makes reduction levers visible.

With our software solution Network, reporting companies receive primary data directly from their suppliers, which flows straight into their scope 3 calculation. A dashboard shows how many suppliers have already provided data and where gaps remain.

Many suppliers, however, lack the resources or knowledge to calculate their Product Carbon Footprints and provide data. ClimatePartner experts guide them through this process – from data collection to the finished PCF – so that reporting companies gain greater transparency over their scope 3 emissions.

Practical guide to scope 3.1 reduction

Scope 3.1 is the single largest line item in the corporate carbon footprint for most companies. Reducing scope 3.1 emissions is challenging, however, because they arise at suppliers, not within your own operations. This guide shows how companies can progressively shift to supplier-specific primary data, reduce scope 3.1, and integrate their supply chain into their decarbonisation strategy.

Download for free