What is the VSME standard?

The VSME (Voluntary Sustainability Reporting Standard for non-listed SMEs) is a voluntary sustainability reporting standard developed by EFRAG (European Financial Reporting Advisory Group) for non-listed small and medium-sized enterprises (SMEs). It was finalised and submitted to the European Commission in December 2024.

The goal of the VSME is to provide a simple, standardised, and proportionate framework for SMEs to disclose sustainability information. It is especially designed to help SMEs respond efficiently to increasing ESG data requests from larger business partners, banks, and investors.

VSME is structured around two modules, Basic and Comprehensive, and is grounded in existing frameworks such as the German Sustainability Code and CDP for SMEs.

The EU Commission officially announced the adoption of the VSME on July 30, 2025.

Why the VSME matters

As sustainability data becomes an integral part of doing business in Europe, SMEs face rising pressure to provide ESG disclosures. The VSME helps SMEs:

- Respond to supply chain data requests

- Improve access to finance

- Align with stakeholder expectations on ESG issues

- Prepare for future regulatory changes

- Reduce administrative costs through a common reporting standard

With the 2025 EU Omnibus proposal likely expanding the relevance of voluntary frameworks like the VSME, more companies than initially expected may find value in adopting it.

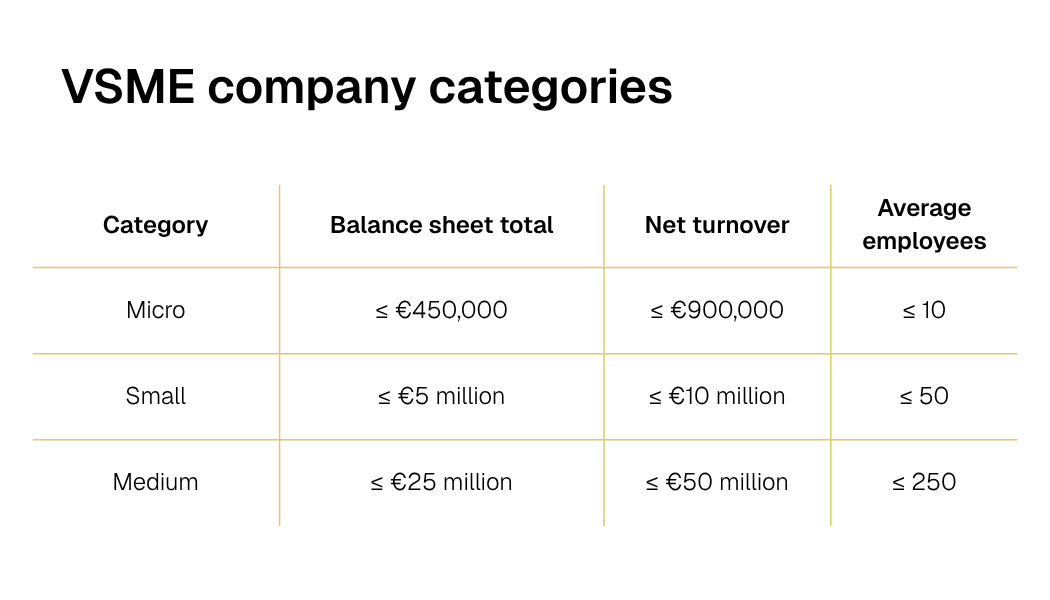

Who can use the VSME?

The VSME is intended for non-listed micro, small, and medium-sized enterprises as defined under Article 3 of Directive 2013/34/EU.

Companies outside the EU or those above these thresholds may also choose to adopt the VSME voluntarily.

VSME structure: Two reporting modules

VSME basic module (minimum requirement)

Covers 11 disclosures:

- General information (2)

- Environmental metrics (5), including scope 1, location-based scope 2, and optional scope 3 emissions (if applicable)

- Social metrics (4)

VSME comprehensive module (optional add-on)

Expands on the basic module with additional disclosures:

- General information (2)

- Environmental metrics (2), including climate transition targets and decarbonisation plans

- Social metrics (3)

- Governance metrics (2)

Companies must always complete the basic module; the comprehensive module cannot be used alone.

Key concept: The “if applicable” principle

The VSME replaces traditional materiality assessments with an "if applicable" principle:

If a disclosure is not reported, it is assumed not relevant to the business. Applicability conditions are clearly stated per disclosure, helping SMEs avoid complex assessments while maintaining transparency.

Benefits of adopting the VSME

- Simplified ESG reporting for SMEs

- Stronger market credibility through transparent disclosures

- Reduced burden from custom ESG data requests

- Improved access to finance, procurement, and partnerships

- Future-proofing against emerging regulation

VSME vs. CSRD and Omnibus

While CSRD imposes mandatory sustainability reporting for large companies, the VSME provides a voluntary alternative for SMEs. With the CSRD threshold for employee size rising from 250 to 1,000 under the Omnibus proposal, the VSME may become the preferred reporting tool for a broader range of SMEs.

Is VSME reporting audited?

No, the VSME is voluntary and does not require audit or inclusion in annual financial statements. However, it can be included in broader sustainability reports if desired.

The VSME gives SMEs a flexible, practical framework to participate in the sustainable transition, respond to business partners, and prepare for regulatory shifts. While voluntary, it aligns with broader ESG expectations and supports long-term competitiveness in increasingly climate-conscious markets.