Corporate Carbon Footprint (CCF) definition

A Corporate Carbon Footprint (CCF) is a structured calculation of all greenhouse gas (GHG) emissions caused directly and indirectly by a company's activities over a defined period, usually a calendar or fiscal year.

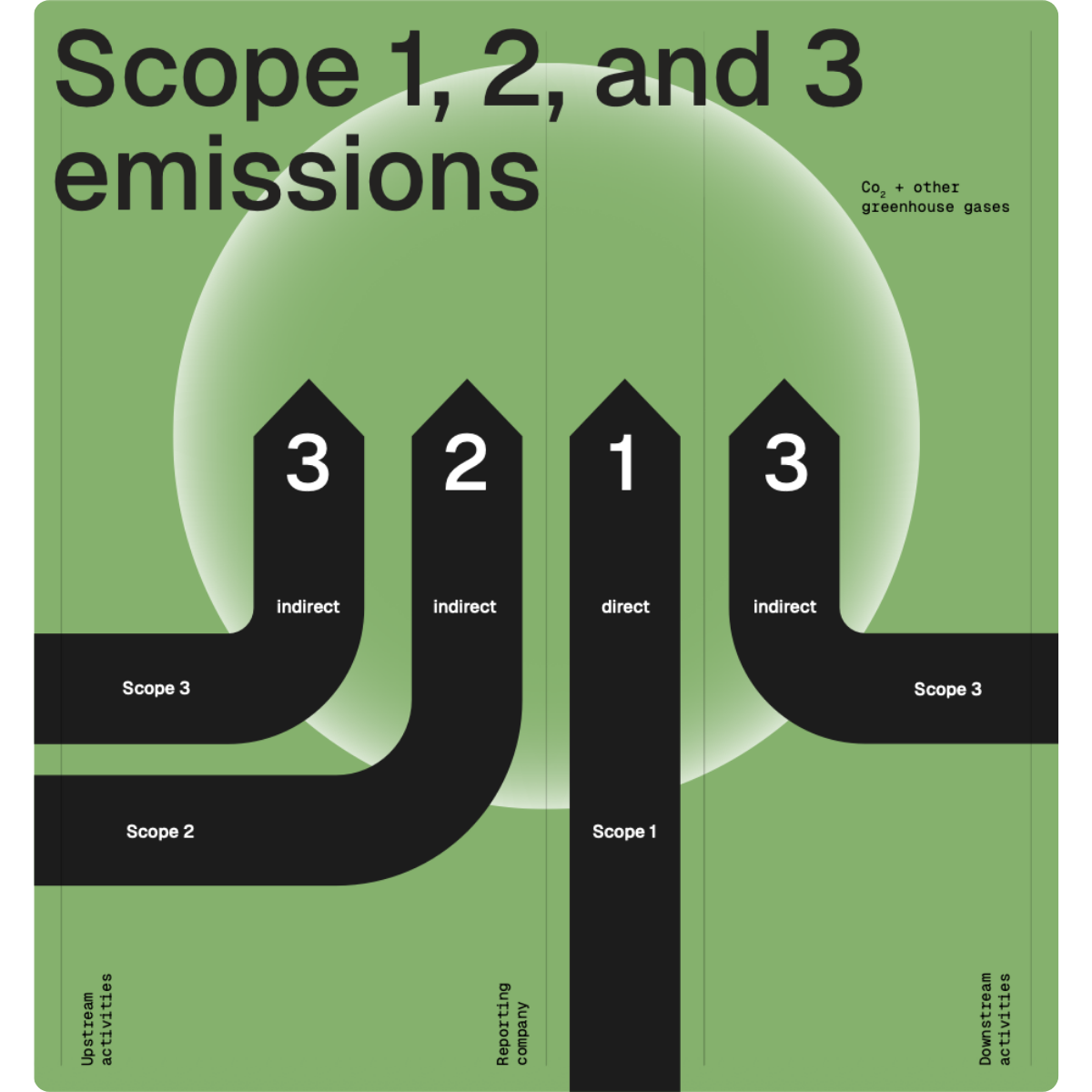

A Corporate Carbon Footprint covers three categories of emissions:

- Direct emissions from owned or controlled sources (scope 1)

- Indirect emissions from purchased energy (scope 2)

- Value chain emissions, upstream and downstream, where in scope (scope 3)

The CCF is the foundational tool for understanding a company's climate impact and forms the basis for strategic decisions on how to reduce emissions and take meaningful climate action.

Why calculate a Corporate Carbon Footprint?

Pressure from legislation, investors, and consumers means businesses must understand and manage their emissions. A CCF provides:

- A baseline for setting science-based reduction targets (SBTi)

- Transparency for stakeholders and regulators

- A clear identification of emissions hotspots to prioritise reduction efforts

- Compliance support for reporting frameworks such as the CSRD/ESRS and GHG Protocol

Only when you know how many emissions your company releases can you assess where to reduce and take action.

How to calculate a Corporate Carbon Footprint: 5 steps

The most widely used framework for calculating a CCF is the GHG Protocol Corporate Accounting and Reporting Standard, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD). Other recognised standards include ISO 14064-1, as well as national and industry-specific methodologies.

The calculation follows five steps:

Step 1: Define system boundaries

Determine which parts of the organisation (organisational boundaries) and which emissions sources (operational boundaries) are included. This means deciding whether the footprint covers the entire company, specific subsidiaries, or individual sites, and which categories across scope 1, 2, and 3 will be calculated.

Step 2: Collect consumption data

Gather activity data across the organisation, such as energy use, travel, procurement, and waste. Primary data generally creates higher accuracy, though secondary or spend-based data can fill gaps where direct calculations are unavailable.

Step 3: Apply emission factors

Match each activity to an emission factor from recognised databases. The emission factor quantifies how much CO2e is released per unit of activity. This step, as well as the next ones, are typically handled by a carbon accounting partner or software platform.

Step 4: Validate and calculate

Check data for plausibility and consistency, particularly when collating information from multiple sites or sources. The validated data is then multiplied by the relevant emission factors to produce the total footprint.

Step 5: Document results

Compile findings into a report for internal and external stakeholders. Required disclosures include:

- Organisational and operational boundaries

- The consolidation approach used

- Total scope 1, 2, and 3 emissions

- Reporting period

- Methodologies applied

- Any exclusions should be documented with justification

Understanding the scopes

The GHG Protocol categorises emissions into three scopes:

| Scope | Type | Examples |

| Scope 1 | Direct emissions from owned or controlled sources | Company vehicles, on-site fuel combustion |

| Scope 2 | Indirect emissions from purchased energy | Electricity, heating, cooling |

| Scope 3 | All other indirect value chain emissions | Purchased goods and services, employee commuting, logistics |

What is mandatory?

Companies must, at a minimum, separately account for and report scope 1 and scope 2 emissions.

Scope 3 is optional under the GHG Protocol but increasingly expected by regulations (CSRD) and target-setting frameworks (SBTi).

| Framework | Scope 3 required? | Deadline |

| GHG Protocol Corporate Standard | Optional (encouraged) | No fixed deadline |

| EU CSRD / ESRS E1 | Mandatory | From 2025 (large companies) |

| SBTi Corporate Standard | Mandatory if scope 3 >40% of total | Upon target submission |

| California SB 253 | Mandatory (US companies >$1B revenue) | Scope 3 from 2027 |

For most companies, scope 3 represents the largest share of their total emissions (often more than 70%).

From CCF to net zero with ClimatePartner

Calculating your Corporate Carbon Footprint is the first step. From there, companies:

- Reduce emissions through science-based targets and operational improvements

- Contribute to certified climate projects for remaining emissions

- Communicate their climate impact transparently to customers and regulators

Start your Corporate Carbon Footprint today.