How does the EU’s omnibus regulation affect the CSRD?

The EU omnibus regulation is a legislative proposal introduced by the European Commission in early 2025 to simplify and harmonise existing EU sustainability regulations. It outlines changes to several key frameworks, including the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), the Carbon Border Adjustment Mechanism (CBAM), and the EU Taxonomy.

The regulation is part of the EU’s broader Competitiveness Agenda and aims to reduce administrative burden for companies by 25% overall and by up to 35% for small and medium-sized enterprises (SMEs). At the same time, it is intended to maintain alignment with the EU Green Deal and support investment in corporate sustainability.

Omnibus changes to the CSRD

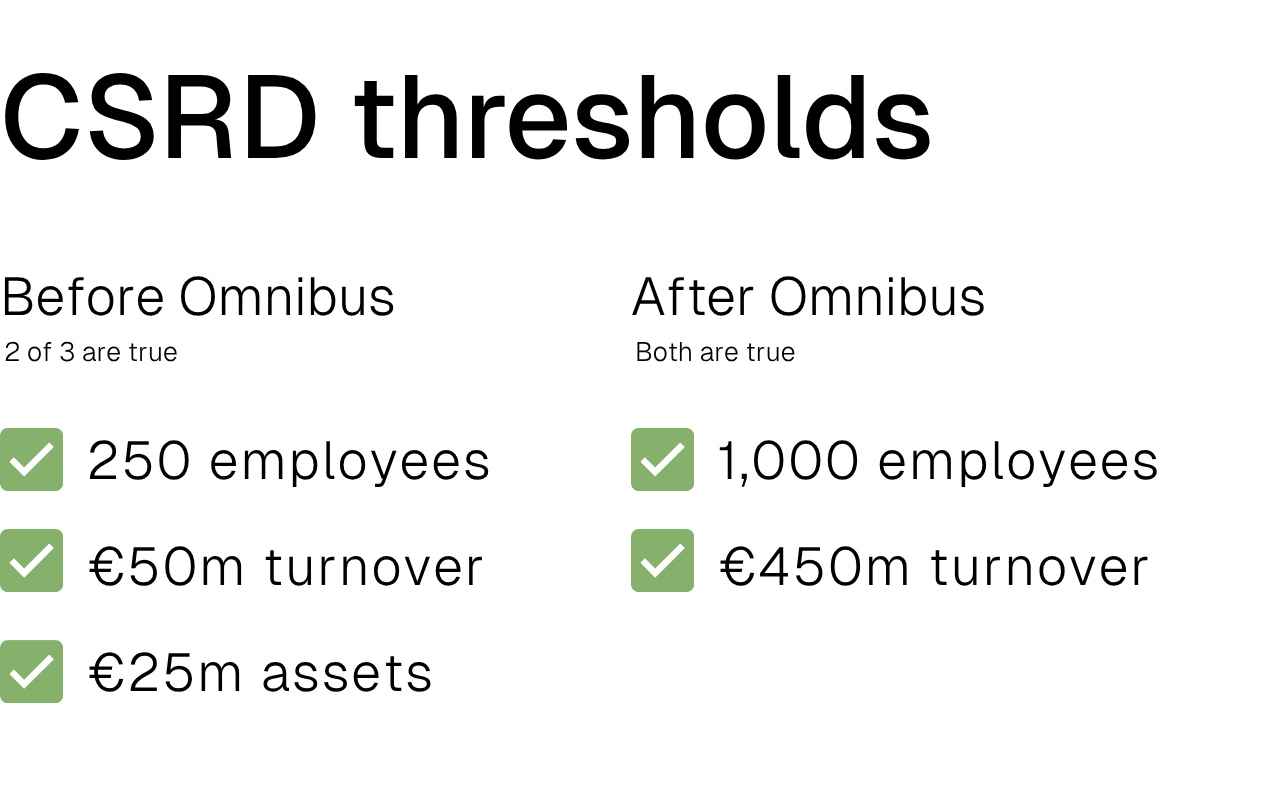

One of the most significant proposed changes in the omnibus is a narrowing of the CSRD and CSDDD thresholds. For the CSRD, only large companies with more than 1,000 employees and net turnover exceeding €450 million remain within mandatory reporting obligations. This adjustment removes around 90% of previously in-scope companies from the CSRD requirements.

For companies that fall below this threshold, reporting remains voluntary. The European Financial Reporting Advisory Group (EFRAG) has a voluntary sustainability reporting standard (VSME) for smaller businesses. This standard aims to help SMEs report essential sustainability data, particularly in response to increasing requests from customers, investors, and financial institutions.

"Stop-the-Clock" proposal of EU omnibus

Approved in April 2025, this "stop-the-clock" proposal delays the implementation timelines for certain reporting and due diligence obligations under the CSRD.

- Wave 2 Companies (large undertakings not yet reporting): Reporting postponed by two years, now due in 2028 for the 2027 financial year

- Wave 3 Companies (listed SMEs): Reporting also delayed by two years, now due in 2029 for the 2028 financial year

- Wave 4 Companies (non-EU undertakings): No change; reporting remains due in 2029 for the 2028 financial year

Simplification of European Sustainability Reporting Standards (ESRS)

The Omnibus simplification sends a mandate to EFRAG to deliver simplified ESRS drafts, which includes:

- Reducing the number of data points

- Clarifying ambiguous provisions

- Eliminating sector-specific standards

Is the double materiality assessment for CSRD affected?

The double materiality assessment (DMA) is not affected by the omnibus. Companies that remain within scope are still required to report both how sustainability factors affect their business (financial materiality) and how their operations effect the environment and society (impact materiality).

Climate action: Beyond compliance

EU regulations like the CSRD are evolving fast, but the strongest business case for climate action isn’t obligation, it’s opportunity. Now is the best time to organise your climate data and prepare for future regulations.

The road ahead may be complex, but inaction is the biggest risk.

Our approach supports both regulatory readiness and long-term business growth through decarbonisation.

Reach out today for more about how we support you.

CSRD and ESRS: How will your business be affected?

With the CSRD, carbon data becomes a crucial reporting element for companies.

Download the e-book to learn whether your company has a CSRD obligation, especially post-omnibus, and what you need to consider for your non-financial reporting.

Download for free