SBTi Net-Zero Standard V2.0:

How to prepare

Get in touch

Updated 11 June 2026

The SBTi Corporate Net-Zero Standard Version 2.0 (V2.0) represents a fundamental shift from climate ambition to climate accountability. Companies that start preparing now will have a significant advantage when it becomes mandatory in 2028. Until then, you can still submit to the current Net-Zero Standard, which remains a strong framework.

Since launching the original Net-Zero Standard in 2021, the SBTi has validated targets for over 11,000 companies, covering around 41% of global market cap. V2.0 builds on that foundation with updated science, tighter rules, and more flexibility where it counts.

Major revisions to the Corporate Net-Zero Standard

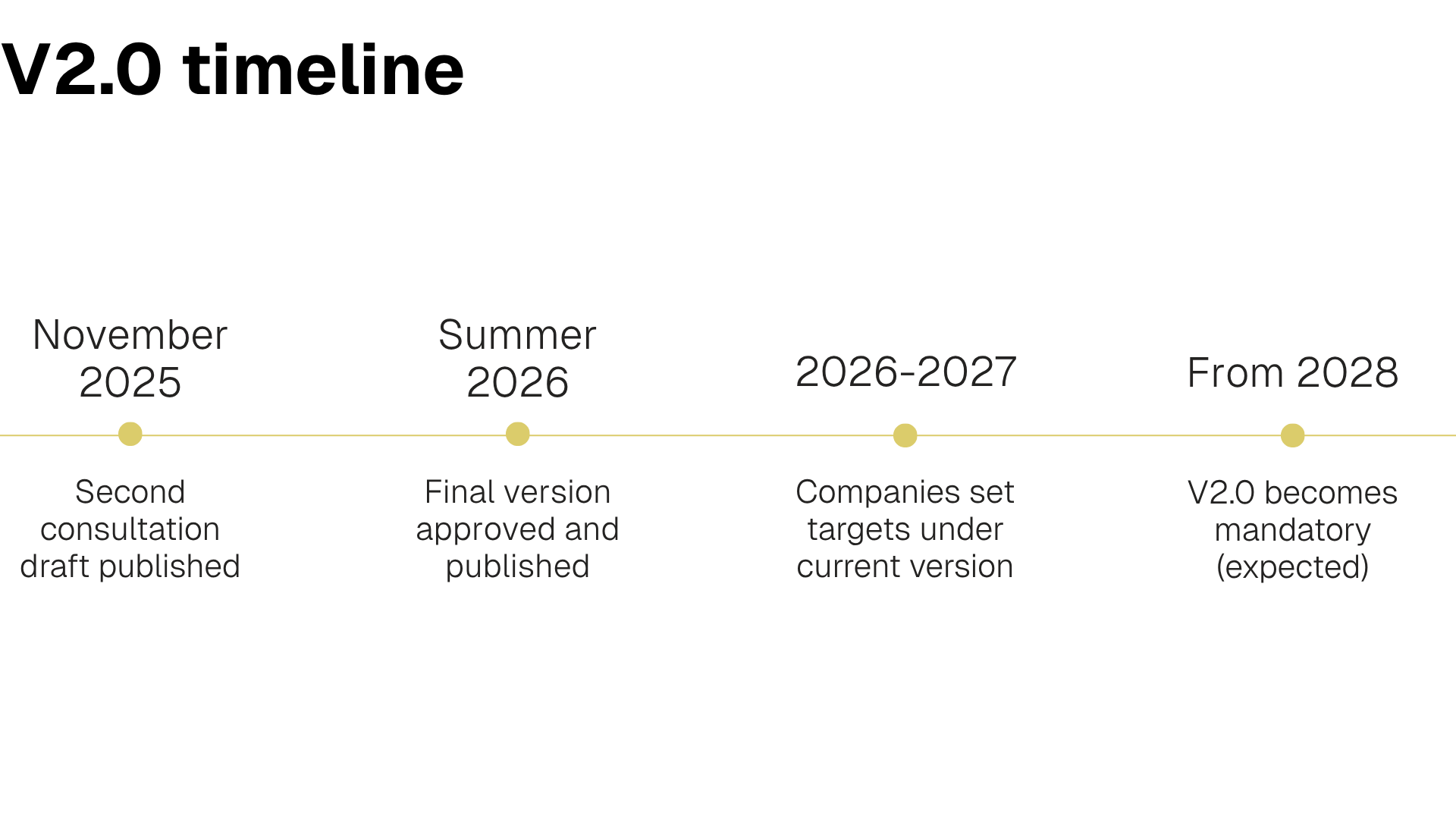

The revision draws on the latest climate science (IPCC AR6, IEA Net Zero scenarios) and is the SBTi's first major update under its Standard Operating Procedures. After two public consultations in 2025, the final version was published on 11 June 2026.

- Scope 1 gets its own target: No more bundling it with scope 2. Companies now have three ways to set a scope 1 target, including methods based on asset replacement and low-carbon transition planning.

- Scope 2 gets stricter: New quality criteria for Energy Attribute Certificates (EACs), and from 2030, the largest consumers (≥10 GWh) are required to report on matching electricity use on an hourly basis.

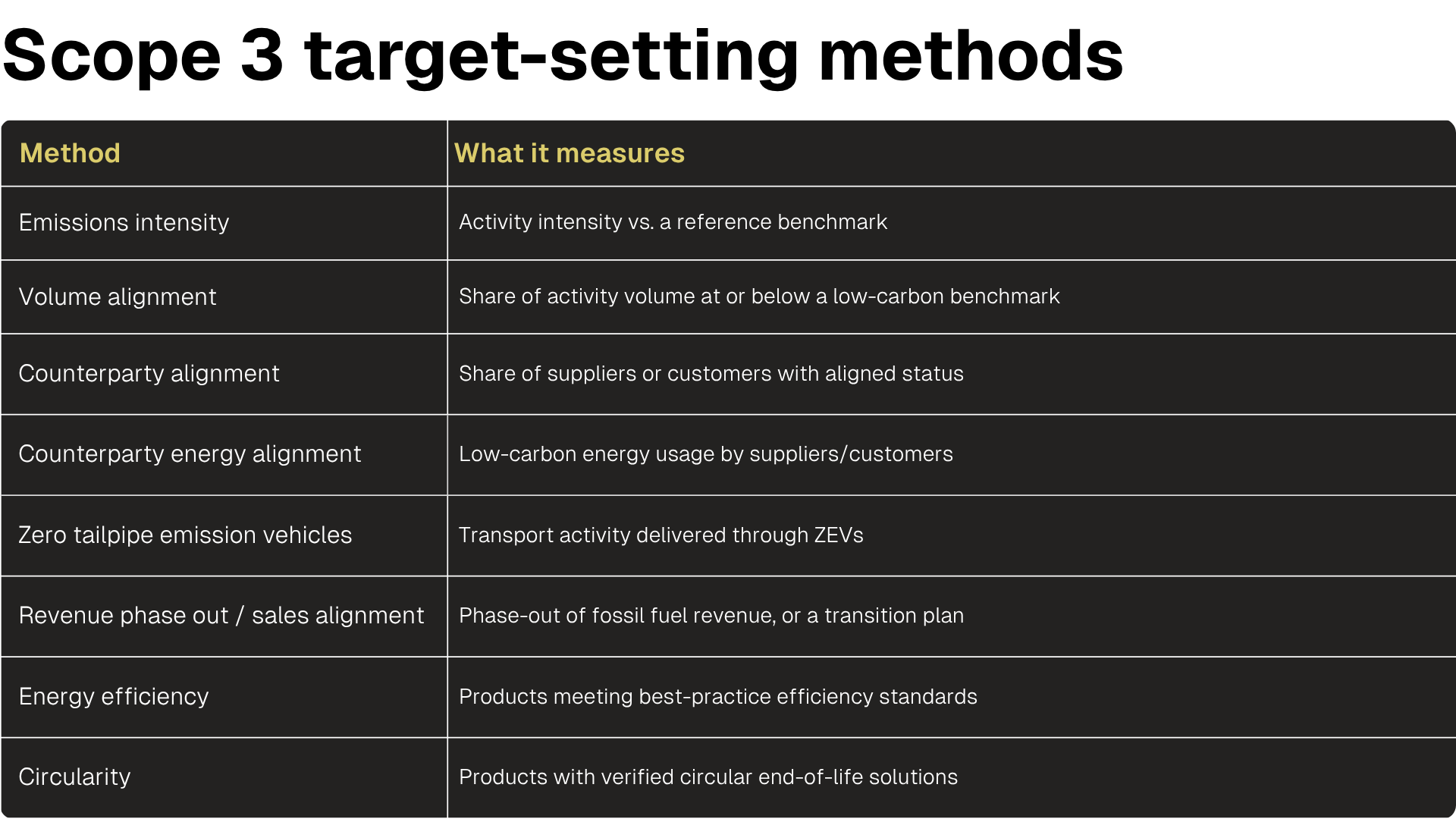

- Scope 3 gets more flexible: Targets now focus on significant categories (>5% of total scope 3), and the menu of methods has expanded from supplier engagement to emissions intensity benchmarks and circularity targets.

- Carbon credits are formally recognised: A new framework lets companies earn public "Engaged", "Advanced", or "Leadership" status based on how they address ongoing emissions.

- Transition plans become mandatory: If you're a larger company (Category A, see chart below), a transition plan is due within 15 months of validation.

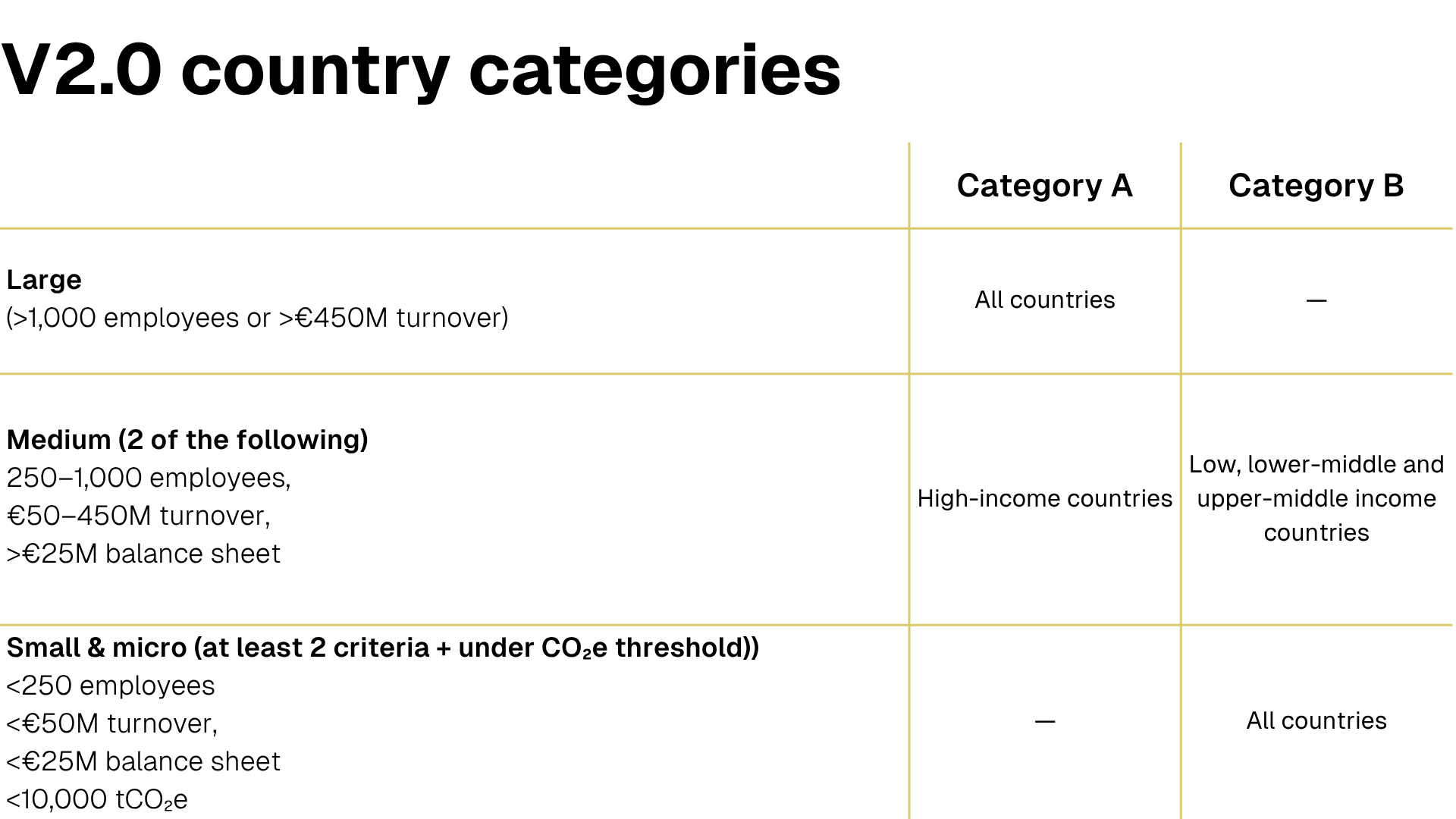

Who does the Corporate Net-Zero Standard 2.0 apply to?

V2.0 introduces two company categories—A and B—based on size and geography.*

*Country classification uses World Bank economic income categories.

Category A companies face the strictest requirements: mandatory transition plans, mandatory responsibility for ongoing emissions from 2035, and mandatory long-term targets for certain methods. For Category B companies: net zero ambitions and transition plans are optional.

The transition timeline: When V2.0 starts

The current Net-Zero Standard remains a credible framework, and targets set under it provide a strong foundation for future V2.0 alignment. Companies can continue using the current version and Near-Term Criteria (V5.3) until 31 December 2027, and existing near-term targets are expected to remain valid until their target year.

Scope 1, 2, and 3:

What's changing

Scope 1: Standing on its own

Under the current version scope 1 and scope 2 targets were typically a combined target. V2.0 scope 1 now stands alone with updated pathways, 100% coverage required, and three methods to choose from:

Linear Contraction

The default. A straight-line reduction rate from base year to net zero. Sectoral Decarbonisation Approaches (SDAs) remain available for intensity-based targets.

Asset decarbonisation

For companies with long-lived assets like fleets or industrial equipment. You set a carbon budget to 2050 with five-year milestones to replace or phase out assets, connecting targets directly to capital planning.

Alignment-based

Tracks the growing share of low-carbon activities over time. Well suited to companies transitioning specific processes, like pairing natural gas with carbon capture.

Scope 2: Higher bar for energy procurement

The primary target method is now an alignment target for low-carbon electricity (below 0.048 kg CO₂/kWh, changing to 0.024 kg CO₂/kWh in 2035), replacing the previous "zero-carbon" framing. Traditional reduction targets using location- or market-based accounting become optional.

EAC quality criteria are also tightening: low-carbon attributes must be generated in the same region as consumption and from 2030, large consumers (≥10 GWh) must begin hourly matching instead of annual totals.

Long-term scope 2 targets are optional for all companies, covering all purchased electricity, heat, steam, and cooling. The goal of 100% low-carbon electricity by 2050 remains.

Scope 3: More focused, more flexible

Scope 3 is where most emissions sit, and where it's hardest to act. V2.0 responds with a framework that's more realistic about how value chain emissions can be addressed.

Targets now focus on significant categories (>5% of total scope 3) and priority emission sources like industrial commodities, fossil fuel activities, and electrified products. Near-term scope 3 targets are required for Category A and optional for Category B.

The methods menu has expanded significantly:

The message is clear: not every scope 3 emission can be traced to a single supplier or solved with a single method. V2.0 gives companies with complex supply chains more credible ways to drive change.

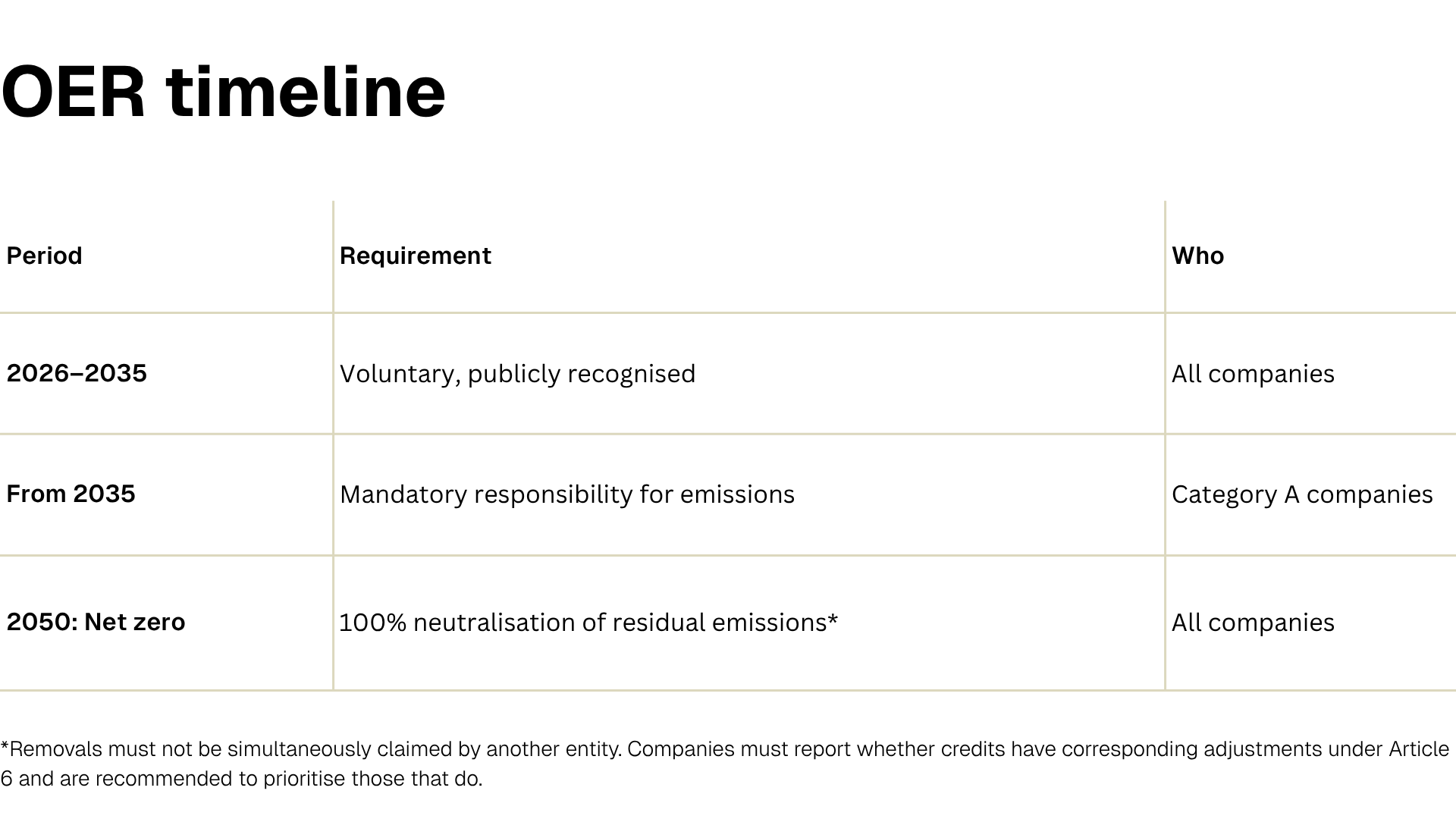

Ongoing emissions: The new carbon credit framework

One of the biggest shifts in V2.0 is how it treats ongoing emissions: the emissions that remain while a company works toward its reduction targets.

The new Ongoing Emissions Responsibility (OER) framework replaces the original Beyond Value Chain Mitigation (BVCM) guidance. Companies that take responsibility for their ongoing emissions could soon earn public recognition from the SBTi.

Engaged recognition level is the entry point: address at least 1% of ongoing emissions, either through verified mitigation outcomes (tonne-for-tonne) or by applying a carbon price (recommended minimum $20/tCO₂e) and directing the budget toward eligible climate action.

Advanced recognition shows that companies measurable climate action: 10% of total ongoing emissions, with a $20/tCO₂e contribution budget or tonne-for-tonne verified mitigation.

Leadership companies goes all the way: apply a carbon price of at least $80/tCO₂e to 100% of ongoing emissions. The remaining budget can support a range of eligible actions: R&D and ex-ante mitigation to adaptation, resilience, and loss and damage finance.

Why early action matters

This framework rewards early movers. Companies acting between 2026 and 2035 earn public recognition now, waiting until it becomes mandatory means missing years of reputational value.

And there's a practical reason too: the removal credit market is still maturing, supply is limited, and prices are expected to rise. Companies that wait until 2035 risk paying more or not securing supply at all.

Why this matters beyond SBTi

Climate science, reflected in the IPCC AR6 and IEA NZE scenarios that underpin the SBTi’s updated pathways, is clear that emissions must fall 43% by 2030 to stay on a 1.5°C trajectory. For many companies, that near-term target year is already approaching.

Even with regulatory shifts like the EU omnibus, the CSRD still references science-based targets, and ESRS E1 aligns with SBTi requirements.

Investors, customers, and supply chain partners, even beyond compliance, increasingly expect SBTi alignment as a baseline for credibility. The direction of travel hasn't changed, only the urgency has increased.

ClimatePartner helps you set targets for the SBTi

Although V2.0 won't become mandatory until 2028, there are ways to prepare now.

ClimatePartner supports you through every stage of the SBTi journey: introductory workshops and emissions hotspot analysis, developing SBTi-aligned near-term and net zero targets across all scopes.

When you're ready to submit, our team prepares the data, provides direct portal support, and handles SBTi queries throughout the validation process.

The complete guide to decarbonisation as business value

Done well, decarbonising lowers costs, reduces risk, strengthens brand trust, and unlocks access to capital. But the path from ambition to action is often unclear, and moving too slowly risks falling behind competitors who are already making carbon reduction part of how they work. This guide shows five ways decarbonisation creates business value and shares cross-sector examples to help you build a plan that fits your resources and operations.

Download for free

Related topics

- What are science-based targets?

ClimatePartner glossary - The case for SMEs to set science-based targets

ClimatePartner blog - Case study: How WAGO Group set science-based targets

Learn more