ESRS E1: Climate disclosure requirements

The ESRS E1 standard establishes disclosure requirements to help stakeholders, such as investors, regulators, and the public, understand a company’s impact on climate change. These include the positive and negative effects of the company, its past, current, and future mitigation efforts aligned with the Paris Agreement, and its plans to adapt strategies and business models for a sustainable economy.

The Corporate Sustainability Reporting Directive (CSRD) mandates non-financial reporting for EU companies, covering environmental, social, and governance (ESG) aspects. Companies must adhere to specific "European Sustainability Reporting Standards" (ESRS), with ESRS E1 focusing on climate change.

The European Financial Reporting Advisory Group (EFRAG), which drafted the ESRS before the European Commission adopted them as a delegated act in July 2023, revised the standards following the EU’s omnibus decision in 2025 to “simplify” and delay reporting for companies. EFRAG submit the revised draft of standards to the European Commission in November 2025, and the EC adopted the revised standards July 2026.

The amended ESRS E1 removes redundant data requirements, emphasises transition planning, climate risk analysis, and emissions reporting, and offers flexibility when value chain data is difficult to obtain.

However, the standard remains focused. When climate change is material, companies must still present a credible transition plan, targets, and a clear link to financial decision-making.

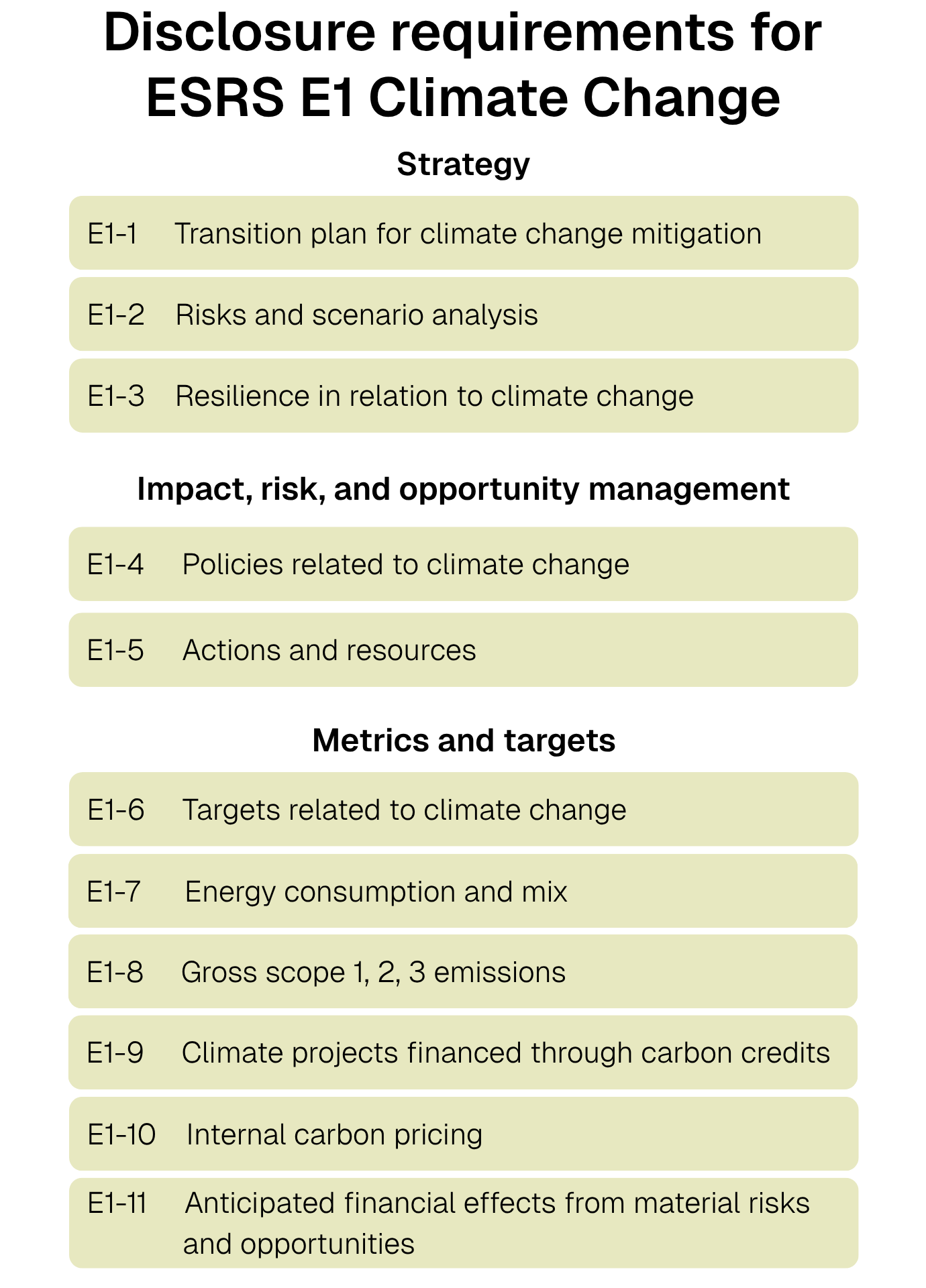

11 reporting requirements for ESRS E1

The amended ESRS E1 includes two more disclosure requirements and the expansion into three sub-sections: strategy, impact and risk, and metrics and targets.

E1-1: Transition plan for climate change mitigation

Providing an understanding of a company’s past, current, and future mitigation efforts. These efforts ensure that its strategy and business model align with the transition to a sustainable economy, the limitation of global warming to 1.5°C in line with the Paris Agreement, and the goal of achieving net zero emissions by 2050. It also includes the company’s exposure to coal, oil, and gas-related activities.

E1-2: Identification of climate-related risks and scenario analysis

This disclosure requirement represents a structural change in the amended ESRS E1. It centres on companies' processes for identifying and evaluating climate-related risks and opportunities through the lens of financial materiality, as well as the rigor of their assessment methodology.

E1-3: Resilience in relation to climate change

Another new change from the amendment, this disclosure requirement addresses the practical implications of climate risk analysis on business strategy and business models. This includes disclosures on climate resilience analyses and their uncertainties.

E1-4: Policies related to climate change mitigation and adaptation

Outlining the extent to which a company has policies in place to identify, assess, manage, and address material impacts, risks, and opportunities related to climate change mitigation and adaptation.

E1-5: Actions and resources in relation to climate change mitigation and adaptation

Disclosing the key actions taken and planned to achieve climate-related policy objectives and targets. Include details of climate change mitigation and adaptation actions, and the resources allocated for their implementation.

The amended ESRS E1 puts more clarity on structures of outcomes and away from action lists that are unstructured.

E1-6: Targets related to climate change

Stating the targets a company sets to support its climate change mitigation and adaptation policies and address its material climate-related impacts, risks, and opportunities.

The amended ESRS E1 added two important updates: emissions reduction targets can’t rely on removals, credits, or avoided emissions, and an absolute emissions value must be disclosed when setting only intensity targets.

E1-7: Energy consumption and mix

Reporting a company’s total energy consumption in absolute value, improvement in energy efficiency, exposure to coal, oil, and gas-related activities, and the share of renewable energy in its overall energy mix.

E1-8: Gross scope 1, 2, 3 GHG emissions

Understanding the gross greenhouse gas (GHG) emissions based on the GHG Protocol:

Scope 1: the direct impacts of your company’s activities on climate change and the proportion of its total GHG emissions regulated under emission trading schemes.

Scope 2: the indirect emissions from energy consumed by your company, whether purchased externally or acquired.

Scope 3: the emissions that occur in your company’s upstream and downstream value chain beyond its scope 1 and 2 emissions. Scope 3 emissions often form a significant part of a company’s GHG inventory and are a key driver of its transition risks.

E1-9: GHG removals and GHG mitigation projects financed through carbon credits

Detailing a company’s actions to permanently remove or facilitate the removal of GHG from the atmosphere, contributing to net zero targets. This includes insights into the extent and quality of carbon credits purchased or planned to purchase from the voluntary carbon market (VCM) to support climate contribution claims.

E1-10: Internal carbon pricing

Disclosing whether a company applies internal carbon pricing schemes and, if so, how these schemes support decision-making and incentivise the implementation of climate-related policies and targets.

E1-11: Anticipated financial effects from material physical and transition risks and potential climate-related opportunities

Outlining a company’s anticipated financial effects from material physical and transition risks, as well as its potential to benefit from material climate-related opportunities.

3 steps for reporting ESRS E1

- Double-Materiality Assessment (DMA): Conducted before reporting begins, the DMA identifies factors your business impacts and those impacting your business.

- Structured reporting: Align your disclosures with ESRS requirements based on your DMA results.

- Independent audit: Ensure your report is independently audited for compliance and accuracy.

The E1 standard aligns with EU legislation and regulations, such as the EU Climate Law, Climate Benchmark Standards Regulation, Sustainable Finance Disclosure Regulation (SFDR), EU taxonomy, and EBA Pillar 3 disclosure requirements, ensuring compliance and consistency in sustainability reporting.

If you would like to learn more about the various ESRS E1 climate change disclosure requirements and our service offerings, please get in touch.

CSRD and ESRS: How will your business be affected?

With the CSRD, carbon data becomes a crucial reporting element for companies.

Download the e-book to learn whether your company has a CSRD obligation, especially post-omnibus, and what you need to consider for your non-financial reporting.

Download for free