CSRD after the Omnibus: Requirements, deadlines, and what to do now

April 14, 2026The EU's sustainability reporting landscape has shifted dramatically. The Omnibus I Directive (Directive EU 2026/470) rewrites the rules on who reports, when, and how much. Here's what the new reality looks like and what your company should do next.

What is the EU Omnibus and how does it affect the CSRD?

The EU omnibus is a legislative simplification initiative published by the European Commission on 26 February 2026. Its goal: reduce the regulatory burden on European businesses without abandoning the EU's core sustainability ambitions.

The directive amends two landmark directives, the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD). The result: narrowed scope, altered deadlines (via “Stop-the-clock" Directive from April 2025), revised reporting standards (expected Q3 via ESRS simplification), and explicit protections for smaller companies in the value chain.

The fast-moving legislative journey:

- April 2025: The "Stop-the-clock" Directive was published, postponing CSRD reporting by two years for large companies not yet required to report (wave 2).

- July 2025: The European Commission adopted "quick fix" amendments to the European Sustainability Reporting Standards (ESRS), allowing companies that started reporting on FY2024 to not have to report additional information for FY2025 and 2026.

- December 2025: The European Financial Reporting Advisory Group (EFRAG), tasked with the European Commission to draft ESRS amendments, delivered its simplified ESRS draft.

- February 2026: The final omnibus directive [Directive (EU) 2026/470] was published, entering into force on 19 March 2026.

- March 2027: EU member states are required to implement draft provisions into national law.

What are the new CSRD requirements and applicability criteria?

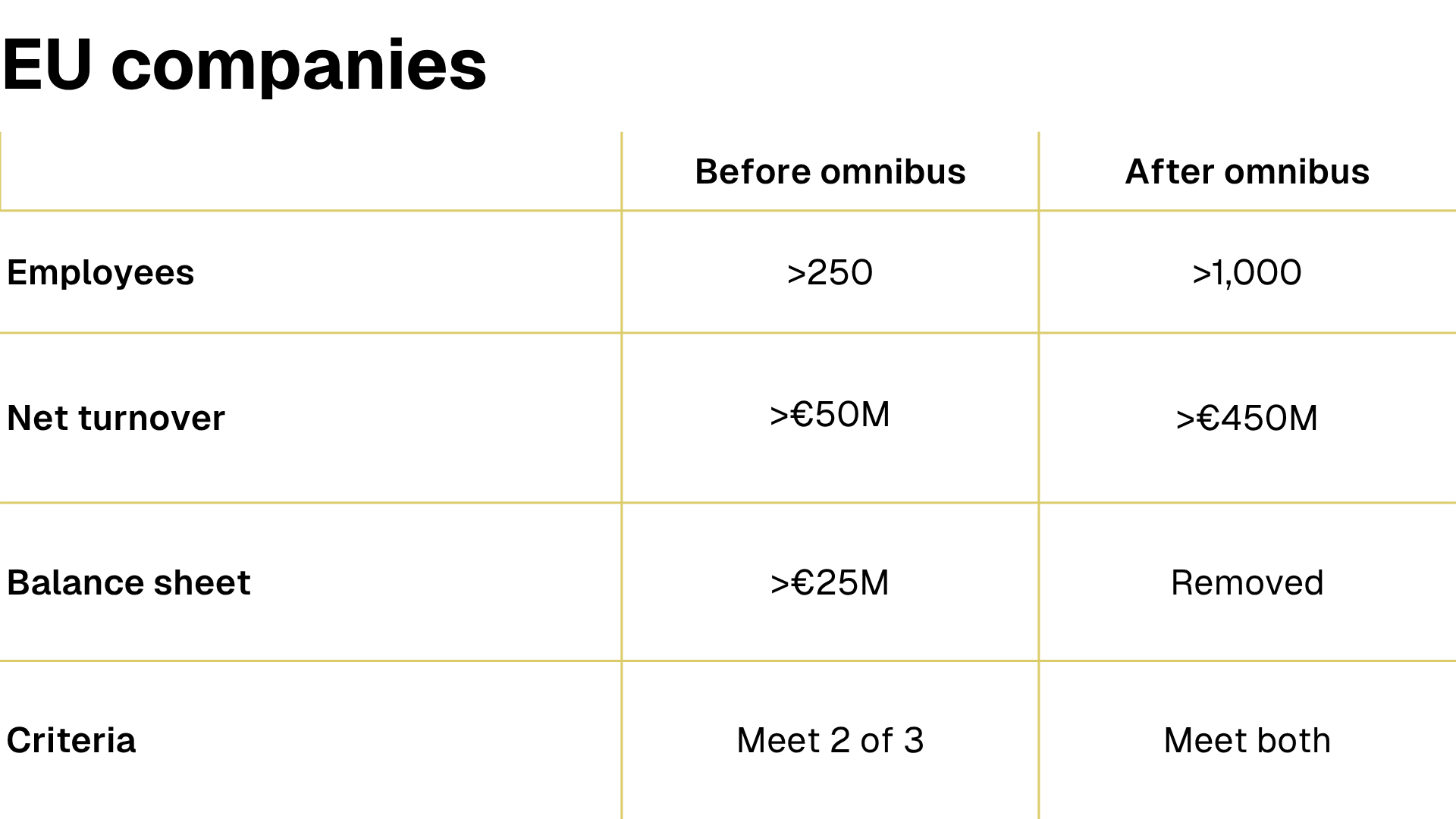

The most visible Omnibus CSRD change is the dramatic narrowing of scope. The original CSRD’s scope was set to cover roughly 50,000 companies across the EU. Under the omnibus, that number drops by approximately 90%, concentrating mandatory reporting on the largest enterprises.

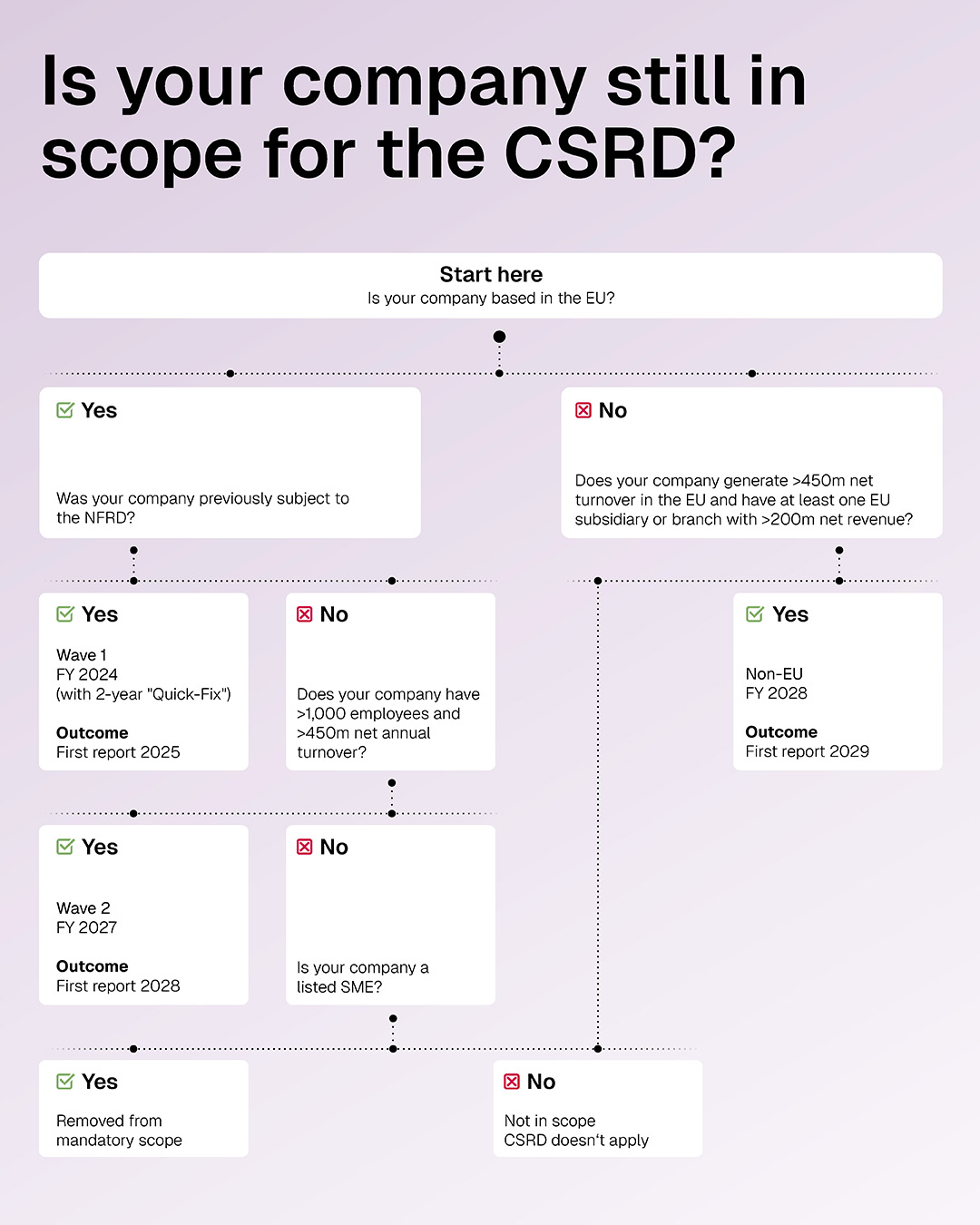

CSRD who needs to report: Is your company still in scope?

Use the decision tree below to quickly assess whether your company falls under the revised CSRD scope.

CSRD timeline for companies post-omnibus

Wave 1: Large public-interest entities

previously subject to the NFRD

First reporting year (data covers): FY 2024

First report published: 2025

The "quick fix" amendements delayed reporting by two years. See leglislative journey timeline above.

Wave 2: Large EU companies

with >1,000 employees and >€450M net annual turnover

First reporting year (data covers): FY 2027

First report published: 2028

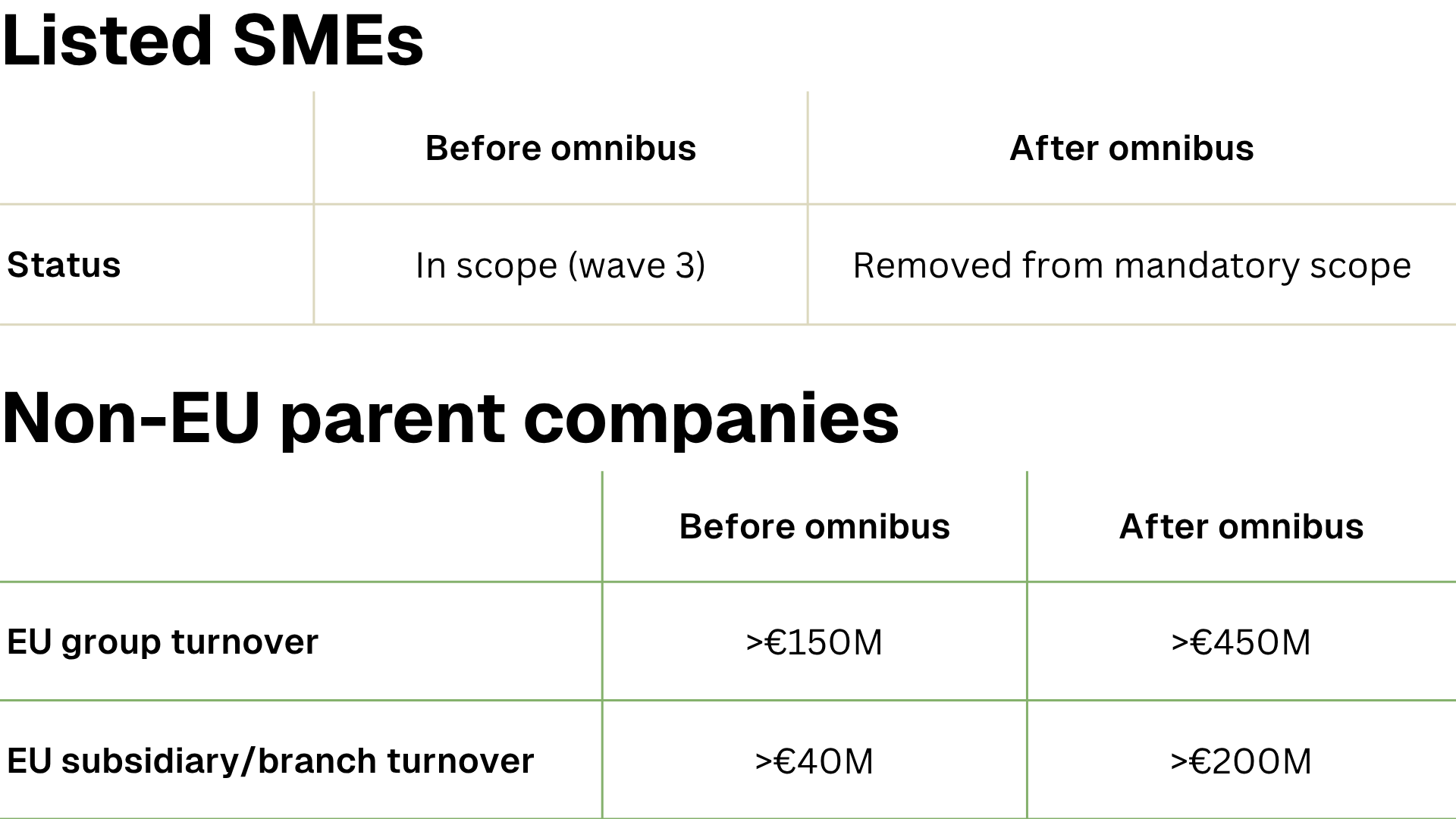

Wave 3: Non-EU companies

with >€450M net EU turnover and at least one EU subsidiary or branch with >€200M net revenue

First reporting year (data covers): FY 2028

First report published: 2029

Listed SMEs

Removed from mandatory CSRD scope. May report voluntarily using the simplified Voluntary Sustainability Reporting Standard for SMEs (VSME) standard.

CSRD disclosure requirements: What happened to the ESRS?

The ESRS have been substantially streamlined but not scrapped. The core remains: companies in scope still report against topical standards (E1–E5, S1–S4, G1) based on a double materiality assessment (DMA). What changed is the volume and granularity of what's required.

Key ESRS simplifications

Fewer data points. EFRAG's amended ESRS reduces mandatory datapoints by 61% and 71% overall when voluntary items were removed.

No sector-specific standards. The European Commission is no longer empowered to adopt binding sector-specific reporting standards. EFRAG continues to develop sector-specific work at a technical level, which may take the form of voluntary guidance, though the exact format and timeline are still undetermined.

DMA still required. The DMA remains the starting point for determining which topics a company must report on, and the fundamental dual-lens approach, assessing both impact materiality and financial materiality, is preserved. However, the revised ESRS 1 introduces simplifications, including a top-down approach to the assessment, a stronger emphasis on the principle of “fair presentation” alongside double materiality, and the introduction of information materiality as a filter for individual data points.

ESRS E1 (Climate change) retains its special status. While data points within ESRS E1 have been reduced, it remains the most substantive topical standard. It is the only environmental standard that keeps its own dedicated anticipated financial effects requirement (E1-11), due to the need to distinguish between physical and transition risks. For E2–E5, these disclosures have been centralised into ESRS 2 (SBM-3).

Simplified ESRS Delegated Act expected by mid-2026. The new standards are expected to apply from FY 2027 onwards, both for wave 1 companies that remain in scope and for wave 2 companies entering CSRD reporting for the first time. In the interim (FY 2025–2026), wave 1 companies benefit from “quick fix” transitional reliefs that effectively freeze additional reporting requirements until the simplified standards take effect.

In practice, the reporting is lighter, but the strategic substance, understanding your climate impact, setting targets, and disclosing progress, remains firmly in place.

What about companies no longer in scope?

If your company falls below the new thresholds, you are no longer required to report under the CSRD. But that doesn't mean sustainability reporting disappears from your agenda.

The VSME standard offers a voluntary path. Developed by EFRAG, and adopted as a Commission Recommendation in July 2025, the VSME provides a framework for companies outside mandatory scope. It includes two tiers: 1) a Basic Module covering core environmental, social, and governance metrics, and 2) a Comprehensive Module for companies that want to go further.

Supply chain pressure doesn't disappear. The omnibus introduces the concept of "protected undertakings": companies with fewer than 1,000 employees that cannot be asked for information beyond what the VSME standard covers. But it also means that the VSME effectively becomes the de facto baseline for what large customers, banks, and investors will request. Companies that proactively report against the VSME will be better positioned to respond to these requests efficiently, rather than fielding ad hoc questionnaires.

Why climate action still makes sense without mandatory reporting

The omnibus changes the reporting obligation, but not the science of climate change, the expectations of your customers, or the financial logic of decarbonisation.

These are no-regret investments. Whether or not your company falls under the CSRD, the core actions (calculating emissions, setting reduction targets, and implementing decarbonisation measures) deliver business value independent of regulatory mandate:

- Customer expectations: Large companies still in scope need value chain data to complete their own reports. If you're a supplier, having VSME-aligned data ready is a competitive advantage.

- Cost savings: Energy efficiency, waste reduction, and optimised logistics reduce operating costs regardless of reporting requirements.

- Risk management: Understanding your climate exposure, from carbon pricing to physical climate risks, protects your business from financial shocks that regulation alone won't prevent.

- Access to finance: Banks and investors increasingly factor ESG performance into lending and investment decisions. A structured and credible sustainability report strengthens your position.

- Preparation for future regulation: The European Commission is required to review the CSRD thresholds by April 2031, and the scope may expand again. Companies that maintain reporting capabilities today avoid a costly restart tomorrow.

- Talent and reputation: Employees, consumers, and business partners increasingly choose companies that demonstrate credible climate action and not just compliance.

The smartest move for companies exiting mandatory CSRD scope is not to stop, but to redirect: shift budget from compliance overhead to actual decarbonisation. The data infrastructure you've already built (or started building) can power a climate strategy that creates value rather than just ticking boxes.

How ClimatePartner helps with CSRD compliance and beyond

Whether your company is in scope for the CSRD or pursuing climate action voluntarily, ClimatePartner provides the tools and expertise:

ESRS E1 support. For companies in CSRD scope, ClimatePartner's services are designed to deliver the specific disclosures required under ESRS E1 Climate change.

Corporate carbon footprint (CCF). A comprehensive CCF covering scopes 1, 2, and 3 is the foundation both for ESRS E1 compliance and for any credible climate strategy.

Reduction target setting. Setting science-based targets is strongly encouraged under ESRS E1 and often expected by investors and other stakeholders. SBTi-validated targets are a widely recognised way to demonstrate that a company’s targets are science-based.

Decarbonisation strategy and implementation. ClimatePartner helps you move from setting targets to actually reducing emissions, from identifying reduction levers to implementing concrete measures, across your operations and value chain.

Climate projects. For residual emissions that cannot be reduced, ClimatePartner supports companies to financially contribute to climate projects that meet recognised international standards.

The regulatory landscape continues to evolve. Member States must transpose the Omnibus I Directive for CSRD by March 2027, and the simplified ESRS Delegated Act is expected by mid-2026. ClimatePartner monitors these developments closely and updates its services accordingly.

CSRD and ESRS: How will your business be affected?

With the CSRD, carbon data becomes a crucial reporting element for companies.

Download the e-book to learn whether your company has a CSRD obligation, especially post-omnibus, and what you need to consider for your non-financial reporting.

Download for free